Hotels and accommodation outlook

Following the announcement of the winter budget on 17 November 2022, RSM polled 1000 consumers to gauge their sentiment towards discretionary spend in 2023. You can find the full results of our survey here.

There’s no doubt consumers are being hit hard by the current economic climate, with 98% saying they are concerned about the cost of living crisis, and 37% saying they have no money left after paying for food, energy and household bills at the end of each month. Below you’ll find our analysis of how these findings relate to the hotels and accommodation landscape in 2023, and the outlook for consumer demand, inbound travel, business and leisure travel, employment, and rising costs.

Consumer demand for UK breaks robust

Demand for holidays in the UK in 2023 looks set to be strong, with our survey showing largely no change year on year to consumers' plans. 36% of respondents said they plan to take a short break in the UK in the next 12 months (unchanged from 2022) and 28% are planning to take a long-stay break in the UK (down 1% on 2022).

The luxury market looks set to remain largely unscathed, with those respondents who earn over £60K per year being most likely to travel domestically. A whopping 47% plan to take a short-stay break of one to four days, and 46% plan to take a long-stay holiday of five days or more in the UK this year. Across the generations it’s the 35-44 years-olds who are the most likely to travel in the UK for their holidays. 47% of this age group are planning a short break, and 38% plan to take a long-stay break in the UK. Digging into the data further, our survey shows UK holidays will also be popular amongst consumers travelling as a family. 40% of respondents with children are planning to take a short break, and 35% of this group are planning a long-stay break this year.

With the good news that consumers still intend to travel in the UK in 2023, particularly across the latter demographics, hotels and accommodation businesses should be feeling buoyant. However, with a cost of living crisis dragging down consumer confidence, operators will need to work harder than ever to secure share of spend. Paying close attention to customer profile will be key. What do travellers with children need to make their trip as hassle free as possible? And what are the expectations of luxury travellers and the latest trends they want to see? Going back to basics and understanding the customer will be essential to maintaining a competitive edge.

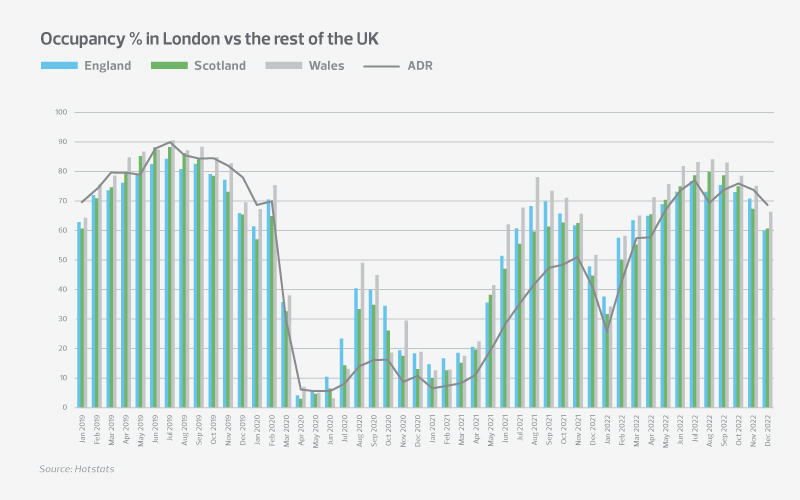

Occupancy will rise year on year

The operating environment in 2023 couldn’t be more different to the climate at the start of last year. In January 2022 consumer’s travel plans were still being hampered by Omicron and other potential Covid variant fears – despite the lifting of all Covid restrictions that month. With no lockdowns looming and consumers still appreciating their newfound freedom, the outlook for occupancy from January onwards in 2023 is more positive.

Indeed, UK hotel occupancy in January last year was down a massive 32% on January 2019 and remained muted in the first few months of the year. However, as consumer confidence to travel returned, we saw hotel occupancy spike in July at just over 77%, which was 25.7% ahead of 2021, and 9.7% behind pre-Covid levels for the same month. This upward curve continued in H2 with performance in December up 18.3% on 2021 and down just 7.1% on 2019. This increasingly positive picture should tick over into January 2023 where we anticipate occupancy will be much stronger and will continue to be so through the first quarter, bringing the sector closer to pre-Covid levels for the year overall.

Inbound travel continues to recover

Also weighing into what we anticipate will be a stronger year for occupancy is the continued recovery of UK inbound tourism. The latest ONS statistics reveal an upward trend in the number of visits to the UK from January 2022 onwards.

Though visits are still behind pre-Covid levels, there’s a pronounced upwards trend, with peak months July and August seeing 3.4m visitors (down 18% on July 2019) and 3.5m visitors (down 21% on August 2019) respectively.

Despite visits not yet reaching pre-pandemic levels, spending by visitors to the UK was promising and much nearer to 2019 levels than we’ve previously seen. Spend for July was £3.1bn by visitors to the UK, which was slightly higher than 2019 at £3bn. In August spend was down 13% from £3.5bn in 2019, to £3bn in 2022, but this still sees visitors spending more per individual than pre-Covid.

The upward trajectory of overseas visitor numbers will continue into 2023, particularly with China opening its borders again. This is good news for corporate focused operators whose recovery has lagged behind the rest of the sector. However, with increased virtual working an enduring theme post-pandemic, it’s yet to be seen if corporate travel will ever recover to 2019 levels.

A continued uptick in overseas visitor numbers to the UK will also boost London’s recovery, where the absence of these travellers impacted businesses most. 2021 was a dire year for London with a lack of international travellers and domestic tourists preferring the UK’s greener spots. However, from June 2022 onwards, with the recovery of inbound travel, London occupancy made a marked uptick and finally overtook the rest of the UK in October. No doubt in 2023 this trend will continue, particularly with big draw events such as his majesty King Charles III’s coronation taking place in London in May.

More generally, demand to travel to the UK is strong. Especially from North America where we’re seeing increased visits aided by the weak sterling and strong dollar. In addition to the coronation, the UK’s hosting of the Eurovision song contest in Liverpool will also give hotels and accommodation businesses another boost from international tourism. In a year where the UK will be doing what it does best – showcasing the depth of our heritage and traditions and hosting large scale international events seamlessly – well-positioned businesses have everything to play for when it comes to capturing share of spend from overseas travellers.

Staff shortages and wages keep biting

It can’t all be good news and staffing certainly caused hotels and accommodation businesses a headache throughout 2022. Getting the right people with the right experience is crucial for the smooth running of hotels and accommodation businesses and historically, European workers have been essential for this. With over two thirds of the UK’s international visitors coming from the EU, the language and understanding skills these workers have, has been important to cultivating a positive guest experience. However, since Brexit and the net migration of many EU workers back to their home countries, there is now a serious skills gap in the market. Not only this, but there is also a lack of desire from UK workers to enter the hospitality industry, due to poor perceptions around careers in the sector.

The latest quarterly labour data released by ONS in 2022 supports this sentiment and showed that in Q4, though vacancies in the accommodation and food services sector had dropped since September 2022 they were still a staggering 41% higher than the comparable quarter pre-pandemic.

Despite a drop in earnings for the sector quarter to quarter, a huge shortfall in staff caused hotels and accommodation businesses to raise salaries in a bid to retain employees in 2022. Earnings were up 23% year on year in Q3 which is the latest available data, and is significant when compared to the UK national average increase of 5%.

Industry data supports these findings with labour costs per available room growing consistently month on month in 2022. This tailed off slightly at the end of the year, but costs were still much higher than in 2019. Typically, labour costs would stay fairly static throughout the year, making 2022 an anomaly. But with demand not looking likely to ease any time soon, and competition for experienced workers still fierce, it’s not likely we’ll see this trend ease anytime soon. Even if the trajectory is more muted when compared with 2022.

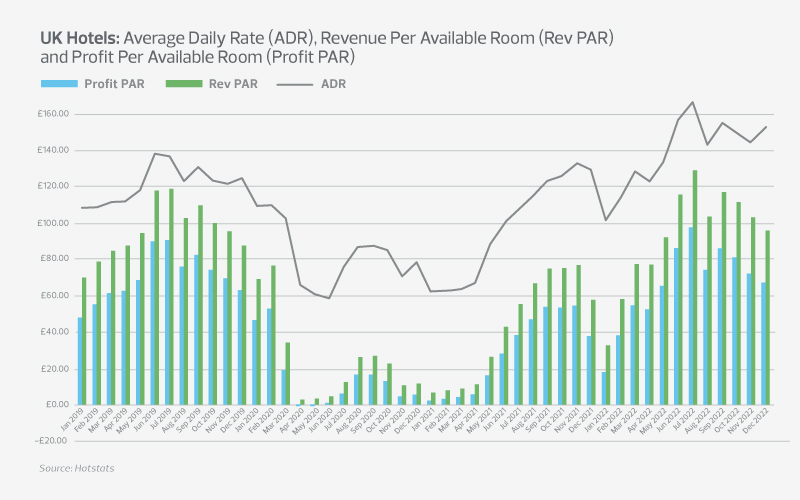

Hotels will continue to insulate themselves from rising costs

Russia’s war in Ukraine and the aftermath of Covid-19 saw global inflation skyrocket in 2022, with UK inflation hitting a 41-year high of 11.1% in October. Consequently, every single UK business has been impacted by alarming rises in their cost base.

Yet hotels have largely been able to insulate themselves from these rising costs. By capitalising on pent up demand from late spring onwards, hotels were able to charge on average nearly 20% more than in 2019 for rooms in H2, which helped them counter headwinds from both inflation and rising staff costs. This saw Rev PAR overreach 2019 levels from July onwards, with some significant jumps in both July compared to 2019 (up £10.09 on the same month in 2019) and in October (up £11.36 on the same month in 2019). Subsequently Profit PAR remained robust even amidst a depressed backdrop.

Indeed, the CPI index showed annual inflation for hotels and restaurants at the end of 2022 was at its highest since December 1991. However, with our survey showing an appetite to travel in the UK in 2023, particularly amongst the wealthy who have space in their household budget to absorb rising prices, we don’t anticipate price increases impacting customer demand by much. Consequently, hotels will continue to pass on inflationary pressures in their cost base to customers in 2023 without weighing on demand.

Insight from RSM UK’s Head of Hotels and Accommodation, Chris Tate:

‘With the end of all Covid-19 restrictions for overseas travellers entering the UK ending only in March 2022, it’s taken longer for the hotels and accommodation sector to get back on its feet when compared with the rest of the UK economy. But after summer 2022, demand came back strongly, and we anticipate this to be a continued theme in 2023, where recovery will come closer to pre-Covid levels.

Luxury and family-focused operators will perform well this year on the leisure side, and as for business travel, recovery here will continue – though it remains to be seen if the sector will ever recover to 2019 levels with the rise of virtual working. The reopening of China should see a boost to both corporate and leisure travel alike and is good news for the sector overall.

Staffing will still be the central challenge for hotels and accommodation businesses in 2023. New initiatives cemented in 2022 to make the industry a more appealing place to work for UK residents must continue if the sector means to turn perceptions around. Equally, staff incentives across the industry will become more competitive as operators do their utmost to retain top talent.

Overall, when compared with other consumer-facing sectors, the outlook is strong for the hotels and accommodation industry, particularly with consumers intending to prioritise discretionary spend on travel. With some flagship events in the calendar including the king’s coronation and Eurovision, the sector has everything to play for and should be entering 2023 feeling buoyant.’

To discuss this analysis, or any business issue you may be facing in the current climate contact our expert:

Related insights

Consumer sentiment mid-year update

04 Jul 2023

Travel and tourism industry outlook

30 Jan 2023

Retail industry outlook

30 Jan 2023

Leisure and hospitality industry outlook

30 Jan 2023

Consumer sentiment mid-year update

04 Jul 2023

Travel and tourism industry outlook

30 Jan 2023

Retail industry outlook

30 Jan 2023