Leisure and hospitality industry outlook

05 February 2024

The hospitality industry endured an ongoing battle with inflation throughout 2023. With like-for-like sales only occasionally beating the consumer price index, meaningful covers growth was off the cards for all but the best in class and instead businesses focused on trying to remain cash flow positive.

Looking to 2024, we anticipate a more positive operating landscape for the hospitality industry. In this article we give the outlook for supply and demand in the sector and identify opportunities and challenges in accordance with the latest economic data and our recent consumer sentiment survey.

Supply side disruption eases but challenges remain

On the supply side, food and beverage costs are well down from the heights of 2022, bringing some relief to operators in terms of margin pressure, albeit energy costs remain around twice as high than they were pre-Covid. Additionally, in April we’ll see the largest ever single increase to the National Living Wage for those aged 21 and over (increasing £1.02 to £11.44) and a similarly sharp increase across other age groups. This indicates that operators aren’t out of the woods yet when it comes to rising costs.

The growing cost of rent, energy bills and ingredients are hitting the independent restaurant sector hard. The start of 2024 has already seen numerous high-profile restaurant closures including Simon Rimmer’s Manchester spot Greens, which shut after 33 years; London restaurant Copper & Ink, run by former MasterChef finalist Tony Rodd; and chef James Allcock’s Yorkshire pub the Pig & Whistle. The first quarter is always a particularly acute time for the sector with lower footfall and the need to pay quarterly rent and higher VAT bills after the Christmas period. We expect further casualties as hikes in National Living Wage and business rates from April make more businesses unviable.

In more positive news, staffing issues are easing and vacancies in November were up 30% compared to pre-pandemic. Though high, the industry is a world away from January 2023 when vacancies were up 55% on pre-pandemic levels and some operators were forced to dictate opening hours around staff availability. Following the talent exodus post-Covid, the industry has worked hard to improve company culture and offer a positive working environment for employees. With perceptions towards jobs in hospitality improving and unemployment ticking up this year, we anticipate vacancies to decline in 2024 and staffing pressures to continue to ease.

Outlook for demand improves as consumer finances recover

In 2024, we’ll see more robust like-for-like cover growth as the outlook for demand improves, particularly in the second half of the year when inflation is forecast to fall to the Bank of England’s target rate of 2%. Interest rates will begin a downward trajectory from summer and are forecast to hit 3.9% by the end of the year. Additionally, real wages will continue to grow this year and with tax cut announcements looking increasingly likely in March’s Spring Budget, these factors should culminate in making consumers feel better off overall. But what’s the outlook for demand by market segment?

Pubs to prosper in 2024

In 2023, pubs emerged as top performers in the hospitality industry, favoured by consumers for their value-driven offering. This trend is expected to continue with consumers planning to increase their frequency of visits to these venues by 11% in 2024. As cost-of-living pressures continue to characterise the first half of the year, pubs will benefit from consumers seeking value amidst ongoing financial pressures. Assuming a more favourable summer this year following 2023’s washout, pubs should thrive as patrons enjoy beer gardens and major sporting events such as the Euros. Added to this, the pub industry, like the rest of hospitality, will benefit from a boost to consumer confidence at the back end of the year as inflation normalises and interest rates begin to fall. Pubs are poised to wrap up 2024 on a high note, marking a resilient year ahead for the sector.

Pubs will benefit from changing consumer behaviours this year. Gen Z, one of the groups most affected by the living costs crisis - especially students - plan to increase their visits to pubs by 7% in 2024. Even with all other demographics planning to marginally decrease their visits to these venues, the increased popularity of pubs amongst younger age groups gives these venues an opportunity to target this growing consumer base with their marketing strategies. With 27% of Gen Z aiming to cut their eating and drinking expenses by looking for special deals and discounts, this is a key opportunity that pubs can leverage.

Older consumers offer a lifeline to the nighttime industry

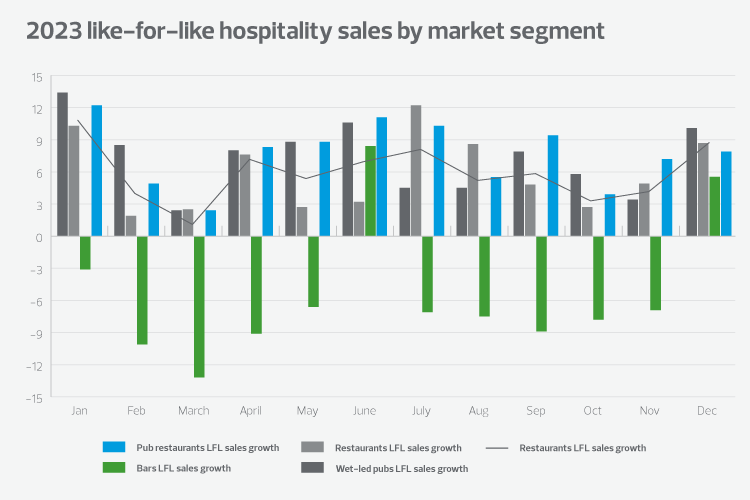

Like-for-like sales for late night bars were down on average -5.5% in 2023, showing the nighttime industry’s continued challenges following Covid-19 lockdowns and cost of living pressures. Revolution Bars, a major operator in the sector, recently announced that it plans to close eight of its least profitable bars this year, an example of the challenges facing the sector.

Unfortunately, the outlook for this year doesn’t bode much better with our recent survey indicating consumers intend to visit late night bars 15% less in 2024 with visits to nightclubs flatlining.

One of the big issues bar and nightclub operators will face in 2024 is the change in consumer habits amongst younger consumers. Where pubs are benefitting from an uptick in frequency of visits from Gen Z and student consumers, this same demographic plan to reduce visits to bars this year by 31% and to nightclubs by 4%. Where pubs represent value to cash-strapped youngsters, bars and nightclubs typically offer a more premium experience with a higher cost attached, which is proving unattractive in the current economic climate.

But there’s a glimpse of light for the nighttime industry in the form of older consumer demographics. Gen X indicate they want to increase their visits to late night bars by 13% this year and Millennials plan to go clubbing 6% more than in 2023. With new concepts coming to the market like Annie Macs ‘Before Midnight’, a 7pm – 12am club night for consumers that ‘need more sleep’, 2024 might be the year we see a shift in nightlife concepts targeted at older consumers who still want to party.

Family-friendly restaurants win-out

Restaurants will see consistent demand in 2024 and will benefit most from high earning households (over £80K per year) and affluent families – those aged between 25 and 54, who have children and have a household income of over £60K per year. These consumers will visit restaurants more than twice as regularly as the average consumer (more than twice a month) and both groups intend to increase the frequency of visits this year.

With 1.6 million consumers due to renew their mortgages this year, concerns around high interest rates will influence the spending intentions of many consumers. Affluent families in particular are set to be one of the most impacted groups, with 93% saying rising interest rates will affect their discretionary purchases in 2024 and will be the main factor influencing their spending over the next 12 months.

So how can restaurants attract and retain this valuable group of customers? One strategy is to offer loyalty programmes. When asked how they would reduce the amount they spent on eating out in the next six months, 41% of affluent families said they would seek out special offers and discounts. This shows that these families are more interested in finding discounts than the average consumer (26%) and suggests loyalty programmes that cater to this group could help to increase customer loyalty and engagement.

Pizza Express is one example of a restaurant taking action to appeal to families. Throughout January, club members will get 50% off dine-in pizzas after research conducted by the business revealed 82% of UK adults said that socialising with friends and family would help them cope with the ‘January blues’. By offering value through their loyalty scheme, Pizza Express is playing it smart to fill covers during the slowest month of trade for the sector.

The return of London continued

In 2022, as Covid restrictions lifted, London was on the back foot compared to the rest of the country when it came to economic recovery. The return of home workers to the city centre was slow which impacted trade for hospitality operators and saw sales performance at the end of 2022 drag behind the rest of the country. 2023 saw the beginning of the bounce back of London, with sales for the year on average up 8.2% on a like-for-like basis inside the M25, compared to 6.5% up outside the M25.

With more corporates either asking staff to come back to offices full-time, or at a minimum three days per week, operators are gearing themselves up for a further uplift in demand in the capital. This coupled with the continued uptick of overseas tourists is seeing operators trial new formats for their offerings to take advantage of increased footfall. For example, Big Table Group have announced that they would test fast-casual versions of existing brands through the launch of pop-ups and double the footprint of their fast-casual restaurant concept Banana Tree. Additionally, Wahaca will open its first new site since 2018 in Paddington this year. With the continued return of office workers and further prospects for increasing overseas travellers to the UK, we expect 2024 to be a strong year for sales performance in London, particularly for casual dining operators with strong, differentiated offerings.

Get in touch

To discuss this analysis, or any business issue you may be facing in the current climate contact our experts, Paul Newman or Robyn Duffy.

Related insights

Consumer outlook mid year update 2024

04 Jul 2024

Hotels, travel and tourism industry outlook

20 Feb 2024

Retail industry outlook

19 Feb 2024

The consumer behaviours that will define 2024

29 Jan 2024

Consumer outlook mid year update 2024

04 Jul 2024

Hotels, travel and tourism industry outlook

20 Feb 2024

Retail industry outlook

19 Feb 2024