Money for nothing: are you maximising cost recovery?

13 April 2022

Charities and implementing partners face unprecedented headwinds. Traditional sources of funding are under pressure, as a result of falling public donations, reduced government assistance, cost of living belt-tightening, and policy diversification. Organisations are looking to further improve cashflow and protect their current programme funding.

In a sector that already has tight margins, increased overheads and committed costs leave little room for error. Indications are that oversight and investigation activity will also increase now that data can be analysed and investigated. Oversight activities will inevitably result in more administrative burdens.

Some organisations will meet these challenges with job reductions and programme cuts, while others will take a ‘business as usual approach’. With no one right answer, often the source and type of funding can be the deciding factor. This is especially true in cases of restricted funding. Trustees in the UK have a legal obligation to ensure those funds are used as intended – although their decisions can have unintended consequences. Reducing the staff resource budget on a restricted-fund project, for example, can mean that those costs and associated management costs cannot be recovered. This often results in limited or no actual financial benefit, but does increase pressure on the wider finance team.

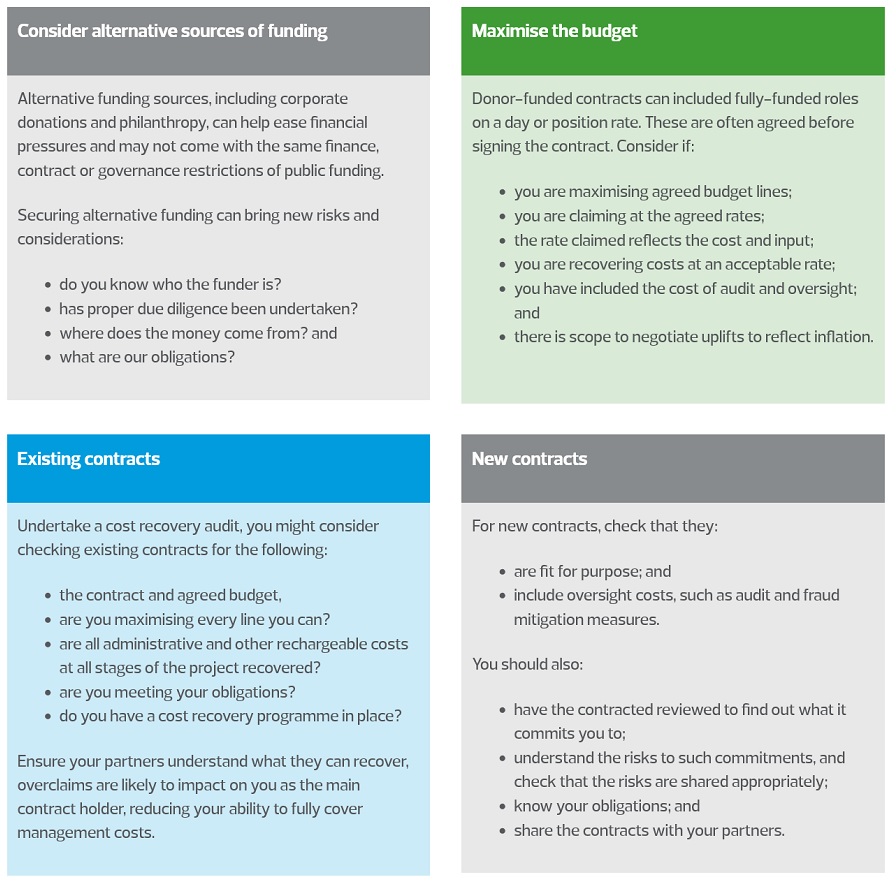

What can you do?

Where employees are included in the budget, confirm that the actual whole employment cost (including on costs and management costs) are reflected in the budget. This will avoid under-recovery of costs. We have found multiple instances where staff and consultant salaries have increased beyond recoverable values in the contract, impacting on the expected cost recovery of the project. Unless it’s a strategic decision to absorb costs, core funding may need to be diverted to cover under-recovery.

Ensure you maximise every direct cost line if the contract has a fixed percentage overhead element. Avoid including direct costs as part of your indirect cost budget.

Have the relevant processes in place to ensure you are not over or dual claiming, as this can bring reputation and funding recovery risk, as well as clawback of funding.

For further information, please get in touch with Mark Sullivan.

Related insights

UK oil and gas policy – a global outlier?

12 Jun 2025

Recruitment sector M&A activity quarterly update

11 Jun 2025

UK oil and gas policy – a global outlier?

12 Jun 2025