UK economy review

RSM UK’s economist, Tom Pugh, examines the economic trends behind market conditions impacting M&A activity in the recruitment sector.

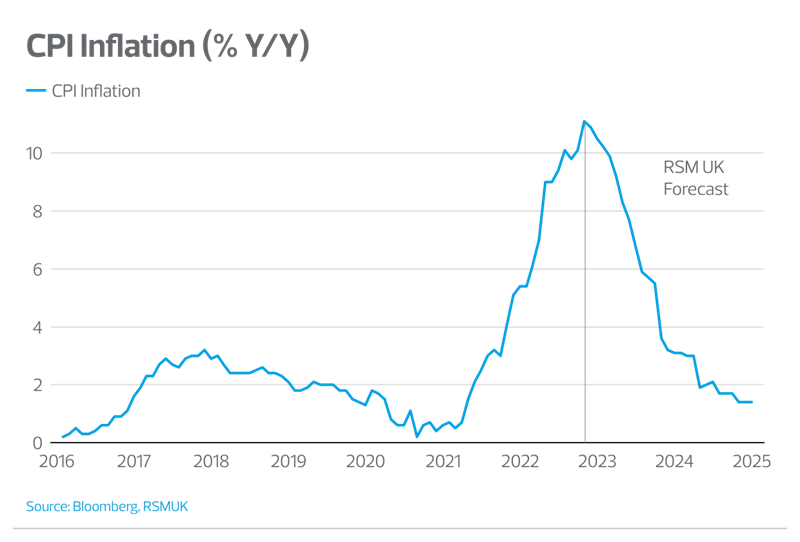

CPI Inflation

We anticipate inflation will continue to fall over the rest of this year. It will likely reach 9% in March – as the fall in commodity prices and shipping costs over the last six months works its way through to prices for food and core goods – and reach around 2% by the end of the year.

Wholesale prices suggest that the CPI inflation rates for electricity and natural gas will slump to about -10% by the end of the year, from their 65% and 129% rates in January. The stabilisation of global agricultural commodity prices over the last six months suggests that food CPI inflation will fall to about 2.5% by the end of this year, from 16.7% in January.

UK recession

The UK has avoided falling into recession by the skin of its teeth, but the worst is yet to come. There are clear signs that the economy has deteriorated over the last few months; GDP fell by 0.5% in December after growing by 0.1% in November. The combination of double-digit inflation, the huge rises in interest rates over the last year and less fiscal support means households real disposable incomes are set to shrink sharply in the first half of this year. That will lead to falling consumer spending and a shrinking economy. As a result, we think the recession has just been delayed, rather than totally avoided.

Of course, narrowly avoiding a recession doesn’t change much on the ground. But a milder recession would mean that unemployment rises more slowly, wage growth stays strong and domestically generated inflation falls at a slower pace than expected. This could result in the Bank of England (BoE) raising rates by more than expected.

We continue to think that GDP will drop substantially in Q1 and Q2. The Government has temporarily stopped paying cost of living grants to low-income households in Q1 and will substantially reduce its energy price support in Q2. What’s more, consumer confidence is still near record lows, which will prevent households from lowering their still high saving ratio.

Meanwhile, the Monetary Policy Committee’s rapid rate hikes have dramatically increased the cost of external finance for corporates, who mainly have floating rate loans.

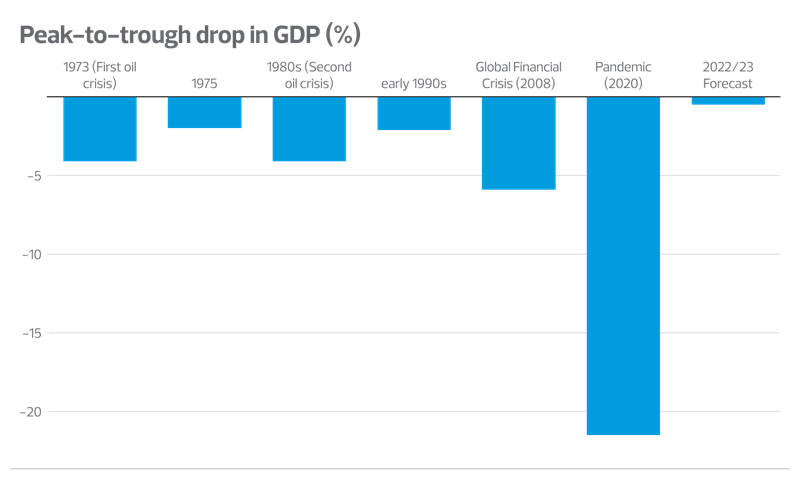

However, the recession we expect in the first half of 2023 will be mild by historical standards. We expect this recession to see a peak-to-trough drop in GDP of roughly 1%. That would be roughly half the size of the early 1990s recession, significantly smaller than the Global Financial Crisis (which had a peak-to-trough drop in GDP of around 6%), and a fraction of the pandemic, when GDP fell by a massive 22%.

Admittedly, the recent collapse in wholesale energy prices suggests that households’ real expenditure will be picking up in the second half of this year and dragging GDP up with it. But the big picture is that the economy could be no larger in 2025 than it was in 2019, before the pandemic.

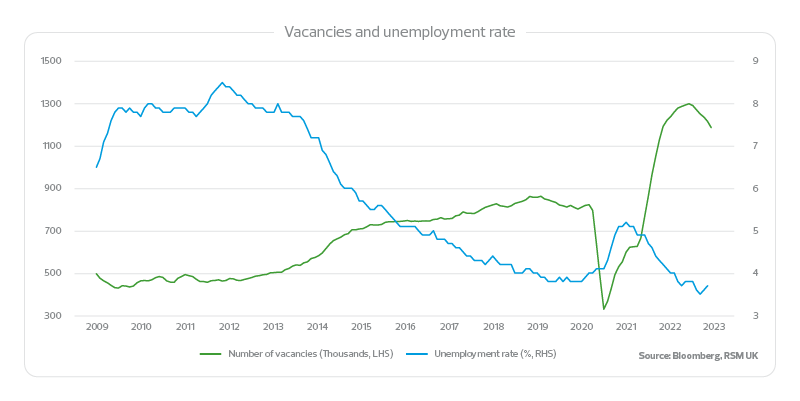

Vacancies and unemployment rate

There are now some reasonably clear signs that demand for labour is starting to weaken. Vacancies continued to fall, dropping by another 76,000 on the quarter in December, the seventh consecutive fall. Most surveys of employment intentions suggest that vacancies will fall rapidly over the next few months.

However, at just over one million last month, job openings remain well above their pre-pandemic average. For now, it appears most firms are adjusting to weaker economic activity by putting hiring plans on ice, rather than making redundancies.

We expect vacancies to continue to fall sharply over the next year as firms reduce their demand for labour. The recession will also raise unemployment levels but, given the surge in the number of people on long-term sick leave significantly reducing the workforce, the unemployment rate is likely only to rise around 5%, a historically low figure, especially during a recession.

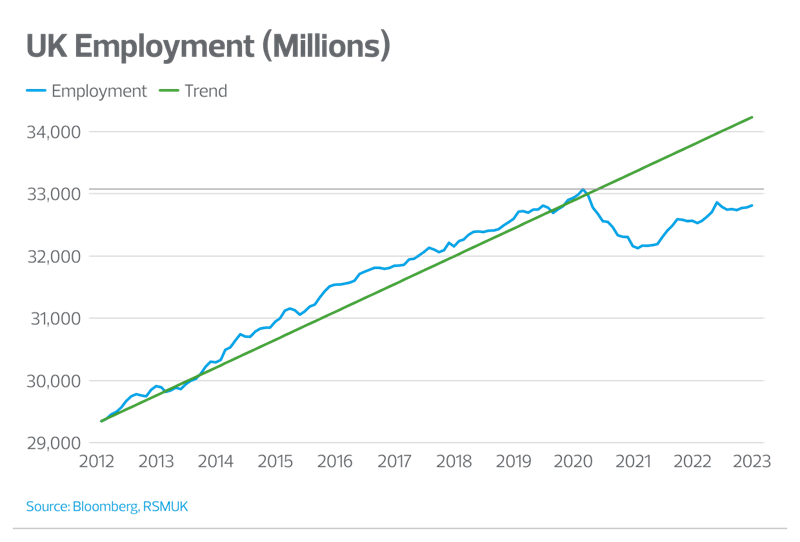

Employment

However, the big issue is still the huge number of inactive eligible workers –- those who have removed themselves from the workforce. Admittedly, inactivity levels have fallen slightly recently. But the inactivity rate was still near its recent high and the shortfall of workers compared with pre-pandemic levels remains sizable, at 280,000. What’s more, there were 843,000 working days lost because of labour disputes in December 2022, which is the highest since November 2011. It will be extremely difficult for economic growth to rebound strongly without getting more people into work.

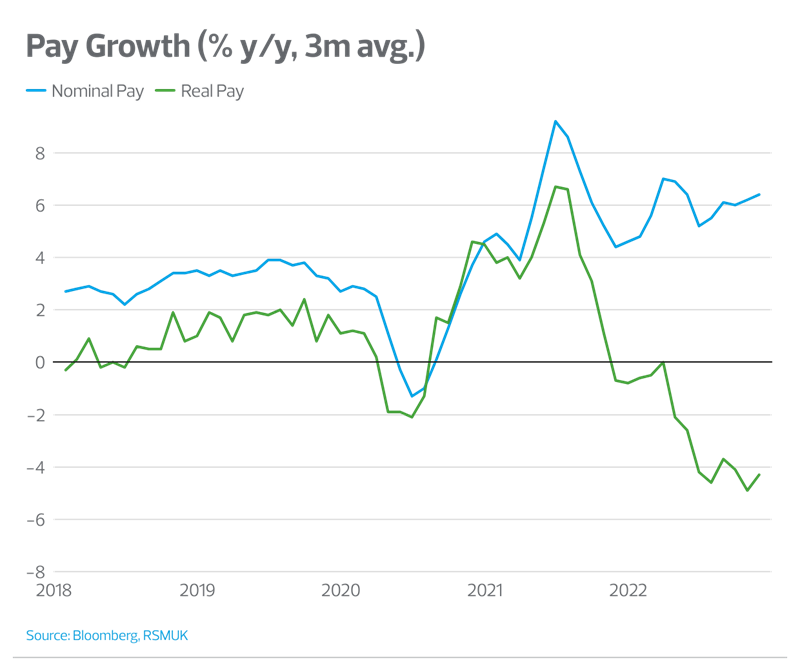

Pay growth and inflation

The tight labour market means growth in regular pay (excluding bonuses) was 6.7% among employees in the three months to December 2022, up from 6.4% in November. This is the strongest growth in regular pay seen outside of the pandemic period – that is, miles above the 3% - 3.5% that’s consistent with the 2% inflation target.

However, it’s not quite as bad as it looks. Average regular pay growth, which the MPC cares more about, was stable at 7.3% and the single month measure dropped sharply in December, suggesting that momentum is waning. Pay growth has probably peaked now. The slowdown in hiring will lead to less churn in the job market, easing the pressure on businesses to pay more to retain staff. However, the Bank of England will want to see concrete signs of easing wage growth before they consider pausing the tightening cycle. That probably won’t be until Q2 this year as the labour market lags the real economy significantly. As a result, the MPC is likely to hike rates by another 25 bps in March, taking rates to 4.25%, where it will probably press pause.

Given soaring inflation, in real terms over the course of the year, regular pay fell by 2.5%, a near-record drop.

For further information and to discuss how this may impact your recruitment business, please contact Neil Thomas, Jonathan Wade, or Clodagh Tunney.