Spring construction outlook: Building resilience amongst the turbulence

25 April 2023

As the economy continues to face challenges with inflation, interest rates and labour shortages, the construction industry grapples further with increased supply chain risk, low margins and procrastinated contract completions and litigation.

CBIL repayments proving difficult

The construction industry was the second highest user of the Coronavirus Business Interruption Loan (CBIL) scheme, designed to provide financial support for small- and medium-sized businesses affected by the Covid-19 pandemic, by helping them access loans up to £5bn.

Due to national lockdowns, businesses were forced to close for six weeks, bringing projects (and their promised income) to a halt. And, once work was resumed, the cost of materials began to rise significantly.

It’s therefore unsurprising that the construction industry accessed significant levels of Covid-19 support funds to address the disruption and the knock-on effect to work practices and global supply chains. However, this has led to significant overleverage within the sector, with the level of debt currently being much higher than historic norms.

In a challenging economic environment this over-leverage has led to many businesses being unable to repay loans, with Construction News reporting that as many as 40,000 construction firms had defaulted on them. This is reflected in the insolvency stats, with construction being the worst-hit sector in 2022 and 4,143 businesses failing over the year. Many high street funders are also stepping back from the industry.

Supply chain troubles rank high in business concerns

In The Real Economy’s latest topical survey, 27% of middle market leaders ranked supply chain disruptions as the biggest risk to their business in the next 12 months and a fifth of the 400 respondents cited concerns at losing key suppliers.

Extended supply chain tiers in the industry results in both the main contractor and key supply chain members having significant risk of sub-contractors failing. To reduce this risk, many businesses are performing enhanced due diligence on their supply chain and reducing the number of preferred suppliers. We have also seen increased collaborative procurement, to reduce risk on the main contractor.

Payment terms through the supply chain have seen improvement over the past two years because of contractors protecting relationships and contract delivery as the supply chain shrinks. This has helped contracts complete without further procurement part-way through. Time taken to pay invoices which was tracking at 45 days on average in 2019, decreased to 37 days in 2022.

Understanding the supply chain’s financial health, as well as scaling capabilities, is key for main contractors and customers to ensure that sufficient cash flow is available for delivery of the contract in relation to timeframes, complexity, and size.

Resilient pipelines, but uncertainty around government spend

After a significant uplift in activity post Covid-19, as contractors played catch up on contract delivery, future activity and new work pipelines saw a fall at the tail end of 2022. However, we can see a small increase in activity in recent months according to IHS Markit and CIPS PMI business surveys.

In 2023 there are early indications of a positive outlook with new orders creeping above 50 – the point which suggests orders are increasing. Our analysis identified pockets of optimism, with the index showing input prices have also stabilised.

While the pipeline activity suggests that work remains buoyant, many of these contracts are delayed government funder projects which were postponed due to uncertainty around plans and protracted mobilisation.

As a low-margin industry which has seen unprecedented material and labour cost uplifts, construction businesses are being particularly cautious when tendering for major and long-term contracts, ensuring contract clauses permit variations of costs while providing some certainty to the customer around contract pricing. 2022 saw many contractors reduce their 2023 and 2024 pipeline as a result of margin preservation and uplift, exiting procurement opportunities and declining tenders where contracts carried too much risk and not enough flexibility around future pricing. This aligned with recommendations in the private sector construction playbook (published in November 2022) to ensure a robust evaluation, risk management and contract selection process.

With increased numbers of insolvencies seen in the industry and contractors being more selective around contract procurement, pipeline has increased, but many major contracts and government projects face the dilemma of minimal bidders.

For a low-margin industry this could have a positive impact long-term on contract procurement and pricing.

Funding long working capital cycles

The construction industry has always struggled to access a wide range of funding options and the complexity of funding long-term contracts has made it tough to ensure appropriate facilities are in place. Recent travails in the sector have only exacerbated the ongoing challenges.

However, a range of new funders have entered the market and, although challenging, there are funding options available to support the construction sector. An example is the housing sector, where new private equity funds are looking to capitalise on the housing demand which, up until early 2023, was seeing an all-time peak in activity and house pricing. The Real Economy’s latest topical survey showed that 47% of middle market respondents expect to use more private equity funding in the next 12 months.

On the back of low margins in 2021/2022, many businesses now face the challenge of shrinking trading activity and pipelines for 2023/2024, making it harder to borrow or to secure funding.

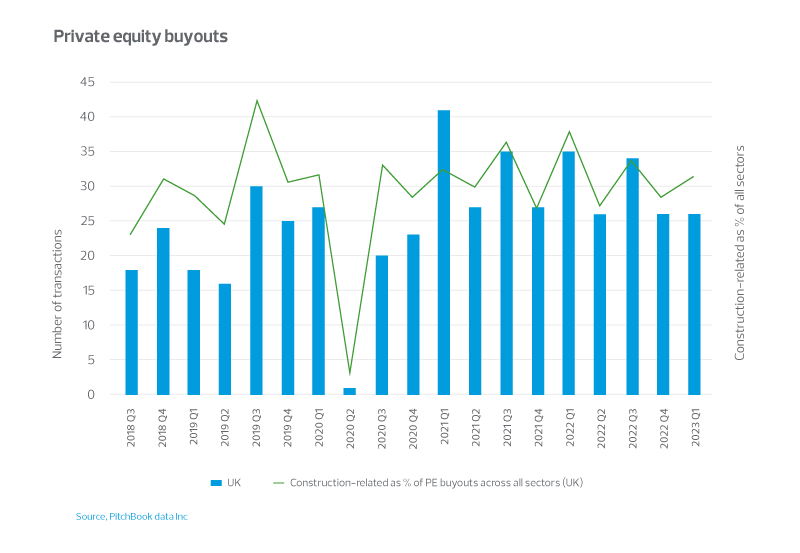

What about private equity investment levels?

Private equity buyout activity, counting platform deals and acquisitions by those platform companies in the construction sector, are ahead of pre-pandemic levels. This is despite rising interest rates which have impacted transaction activity.

There is still lots of ‘dry powder’ to deploy and there is an unmet need for housing in the UK market, which bodes well for attracting equity investment within the sector in future. But economic headwinds will pose a challenge and there remains crucial fundamental aspects that construction businesses will require to attract the investment available. For example, confidence in future revenues, strength of management team, visibility of pre-existing debt levels and profitability.

With the impact of Brexit, Covid-19 and inflation, the industry has seen many contracts originally procured at sensible margins, result in large losses, as labour restrictions and material prices rocketed to unprecedented levels. Some businesses would have had multiple contracts in this position, many with litigation attached. And so, understanding the businesses future performance has been challenging for all funders.

Key considerations for the industry to ensure resilience and future performance:

- retain strong supply chain relationships, performing enhanced due diligence and maintaining payment terms;

- create a robust bid management process, risk assessing tenders and margin performance;

- ensure contract management and reporting is timely and robustly challenged to identify early stages of margin erosion; and

- review working capital requirements, particularly where a business is seeing opportunity for growth in revenue due to on-boarding larger contracts.

While the construction industry faces much disruption and turbulence, it is not all bleak. There are still many significant government-backed projects in the pipeline, and a demand for affordable and family homes in the UK. These opportunities will help return the industry to optimism, and with stabilising material prices, better procurement processes and access to more financial support, this makes for a brighter 2024.

The Real Economy

Subscribe to The Real Economy

Related insights

Private equity: Q&A with Jasper Van Heesch

17 May 2023

Spring retail outlook

26 Apr 2023

The technology layoffs: how did we get here?

06 Mar 2023

Private equity: Q&A with Jasper Van Heesch

17 May 2023

Spring retail outlook

26 Apr 2023