Direct lending – navigating the complexity

27 April 2023

Direct lending remains a key source of capital for private equity backed middle market businesses and will continue to fill a gap as the bank market retrenches. But - it’s a complex market to navigate.

Disruptions to bank debt capital supply and related uncertainty from the likes of Silicon Valley Bank (SBV) and Credit Suisse has led to increased caution from banks. This in turn has led companies and investors actively looking to make transactions to turn to direct lending as an alternative funding option.

Middle market businesses looking to raise capital should be considering direct lending. It’s a funding source that offers advantages, even in a high interest rate environment.

Understanding private credit and when it is used

Direct lending, otherwise known as unitranche loans or private credit, is typically a senior term loan but one that may also include revolving credit lines and second lien loans, the latter being subordinated loans to the most senior (first lien). They are typically issued by closed end funds, i.e. they are not public market capital vehicles.

Many companies and their private equity backers are selecting direct lending over traditional bank financing. Direct lending typically offers more tailored loans and deals executed quickly, making them attractive to certain types of deal seekers. These attributes are particularly useful when portfolio companies pursue a buy-and-build strategy via making add-on acquisitions, where financial backers can move quickly and can be flexible with regards to the amount of debt required.

However, many companies select this type of debt through necessity. The 2008 Global Financial Crisis led to heightened regulatory requirements and balance sheet restrictions on banks, forcing them to focus on lower risk investments.

The consequence of this change is that syndicated bank loans are now typically aimed at larger deals. In fact, the direct lending market hardly existed before the crisis. Higher risk debt providers took the chance to fill the gap for middle market companies.

As ‘take-and-hold lenders’, direct lending funds have provided greater certainty of execution for borrowers in volatile credit markets.

The flexibility, speed, certainty and higher risk profile of direct lending does, however, come at a cost. These deals come with higher interest rates – typically 2 to 5% higher - than bank debt.

The pros and cons of direct lending vs. bank loans:

- Pros:

- Speed of execution

- Flexibility in terms of financial and non-financial covenants

- Certainty of execution in volatile credit markets

- Bullet maturities (the repayment at maturity of a one-time lump-sum or a disproportionately substantial portion)

- Cons:

- Higher interest rates

- Early prepayment penalties

Private debt fund raising: still significant, but coming under pressure

In 2022 fund raising of private debt, which direct lending is a part of, was still significant by historical standards, with $200bn raised on a global basis, according to PitchBook Data Inc. This was the second highest of all time, with $250bn raised in 2021. This took the global private debt dry powder pool to $395bn, or 2.2 years of cash on hand.

Private debt fund raising has seen significant growth, with direct lending the largest portion

The range of focus areas demonstrating that this source of capital can be used in a variety of situations other than just for leveraged private equity buy-outs, as demonstrated by the top four categories of 2022’s fund raising, as follows:

- Direct lending made up the largest share of the private debt funds raised in 2022, at 37% ($74bn)

- Mezzanine (subordinated debt, generally with features similar to preferred equity, such as warrants and often used in buyouts, 20%

- Credit Special Situations (debt or structured equity investments made with the intent of gaining control of a company, generally one in some type of financial distress), 14%

- Distressed Debt (traded debt instrument of companies in distress),12%

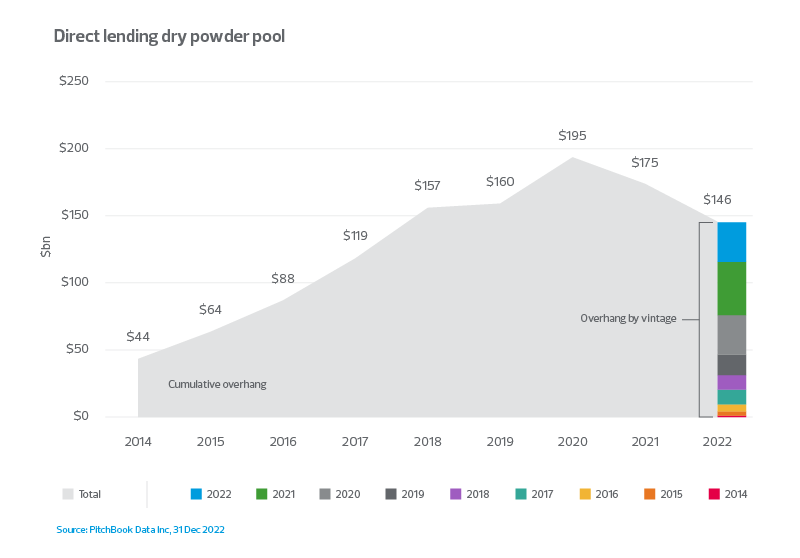

Significant direct lending dry powder still available

Direct lending fund raising has seen a steep rise since it first appeared after the Global Financial Crisis.

It did see a drop of 48% between 2021 and 2022, resulting in the direct lending dry powder pool dropping from a peak of $195bn in 2020 to $146bn at the end of 2022, a 25% drop over those two years.

However, that’s still a significant figure and the fourth highest at year end.

Looking into 2023, the rating agency KBRA suggests that Q1 of 2023 will be one of the slowest quarters for direct lending. New-issue volume in January was $8.8bn. But, if the massive $5.5bn financing by Carlyle Group related to the acquisition of the healthcare technology firm Cotivity is stripped away then the total raised was only $1.1bn. As a matter of interest, the Cotivity deal is the largest direct lending deal in history.

It’s worth noting however that private equity is still sitting at near record levels of dry powder ($1.24tr at 30 Sep 2022). We expect that dry powder to be deployed in the next 3-4 years and those investors will be seeking out debt solutions to support their acquisitions. In other words, there will be demand for this debt, which should then drive supply.

Other notable features of this debt market

1. Concentration into larger hands, and by geography

There’s an increasing concentration of private debt into the hands of the larger funds. In 2021 there were 330 private debt funds closed.This number was halved in 2022 while the debt raised only dropped by 20%. This concentration is also appearing in the Direct Lending subset.

The lion’s share of private debt fund raising was in the US (75%), followed by Europe (22%).

It’s worth noting that cross border debt provision does happen, but companies outside of these regions will be at somewhat of a disadvantage due to the inherent associated risk, e.g. currency fluctuations.

2. It’s a complex space to navigate, with many providers and covering a range of investment appetites

As there is in private equity, where there is a wide range of investment appetites, the same is true in the private debt market, including in direct lending. In fact, RSM engages with over 100 direct lenders, each offering different terms.

That broad range is a simply a direct reflection of the flexibility that direct lending offers borrowers but the consequence is that a company can spend many wasted hours knocking on the wrong doors, and even end up empty handed.

Debt funds are much more likely to have a binary view – if they don’t like the credit, they will reject it outright, whereas if they do like it, then they will pursue it aggressively. It’s hard to predict how each lender will behave on any given deal. In contrast, banks often feel obliged to put forward terms, even if these are relatively lukewarm, as they manage their relationships.

It’s typical therefore to go fairly wide in a deal backed by debt funding, with advisers usually handling the footwork to secure the right investors.

Direct lending has become a key source of capital for middle market companies with a significant pool available. These investors offer benefits like greater flexibility and speed of execution but companies will need to balance that off against the higher interest rates charged. Every debt deal will encounter complexities but companies that navigate this well will find backers that suit them.

Related insights

Generative AI – fraud friend or foe?

19 Mar 2024

Fraud in Financial Services

13 Mar 2024

Retail Outlook: Golden quarter

07 Nov 2023

Economic crime and corporate transparency bill

21 Aug 2023

Generative AI – fraud friend or foe?

19 Mar 2024

Fraud in Financial Services

13 Mar 2024

Retail Outlook: Golden quarter

07 Nov 2023